Do you receive income or have assets, bank accounts, or properties abroad? Then keep on reading, because most likely you must declare your possessions through the 720 tax form in Spain. In this article you will learn everything you need to know about it. We’ll see exactly what this model is about, how often should you file it, which are its exceptions, how to properly declare your assets, and most importantly, all the monetary penalties that you can face when failing to submit it or when hidding any relevant information. Knowing how this tax form works is essential, so let’s dive into it!

What is the tax model 720?

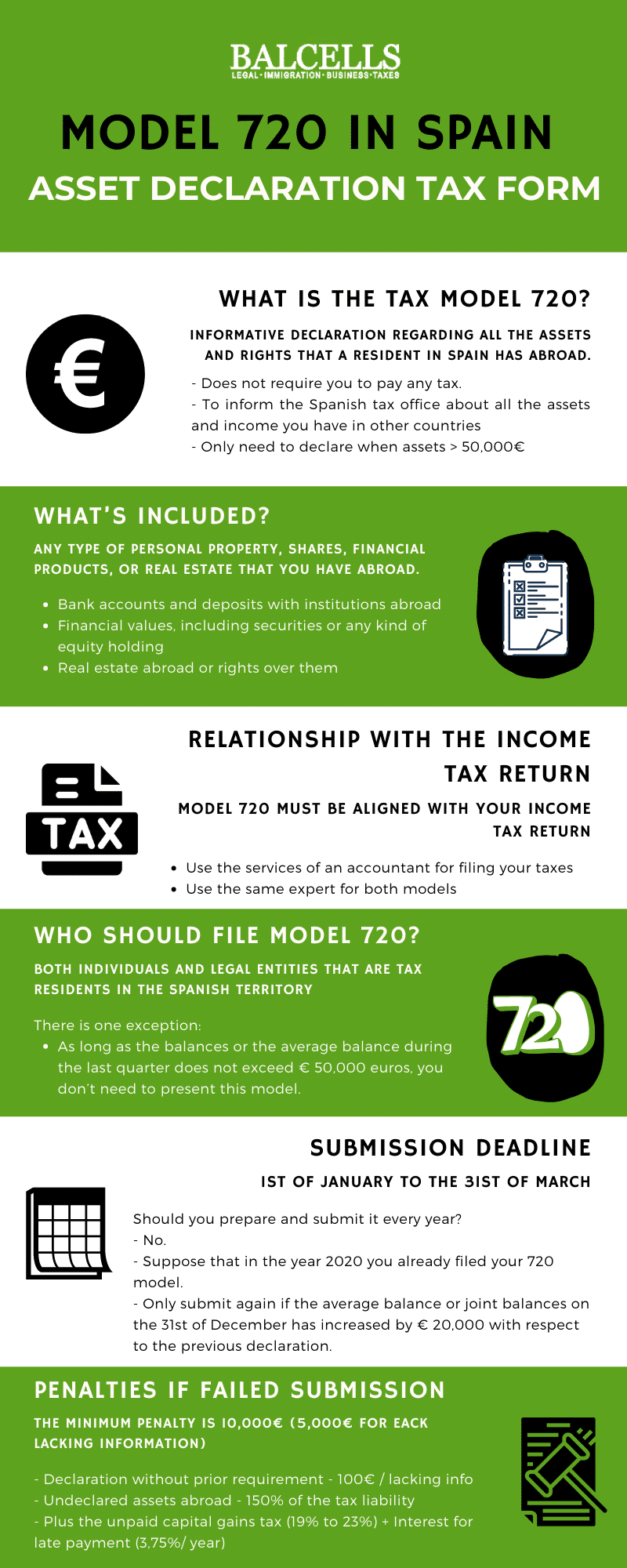

Tax form 720 is an informative declaration regarding all the assets and rights that a resident in Spain has abroad.

We are talking about a declaration done yearly, and the fact that it is a declarative model is a very important detail to consider.

Unlike other tax forms, such as the quarterly VAT declarations, in this case the 720 form does not require you to pay any tax. In other words, its only purpose is to inform the Spanish tax authorities of the assets and income you have in other countries; but this will not involve any direct tax burden (although you will almost certainly end up paying taxes on the income obtained abroad, but not through this model).

Thus, it is intended to inform the Spanish tax office about all the assets and income you have in other countries, whether they are assets themselves or rights over them, securities, any type of insurance, or bank accounts.

In other words, to keep track of your assets abroad and all the assets that generate income and profits, as well as to report their value.

And you will only need to declare those assets or wealth as long as the value or income they generate is greater than € 50,000, as we will see below.

What’s included?

On a general level, this declaration includes any type of personal property (money), shares, financial products, or real estate (such as a house or house rents) that you have abroad (in any country other than Spain).

More specifically it includes three main groups:

- Bank accounts and deposits with institutions abroad

- Financial values, including securities or any kind of equity holding

- Real estate abroad or rights over them

We can see them separately in the following list:

- Bank accounts held abroad

- Securities or equity holdings abroad (e.g. shares in a start-up company)

- If you trade with any type of broker, for example when investing in the stock market, it is most likely that the broker is abroad (hence included in this declaration); or with any cryptocurrency exchange.

- Shares or units in the capital of collective investment institutions

- Securities representing the transfer of personal capital abroad to third parties

- Life insurance when you are a policyholder or an insured person, contracted with an institution in a third country

- Property or rights over a property owned in another country

- Life annuity or any kind of temporary income from abroad

Relationship with the income tax return

It’s really important to mention that model 720 must be aligned with your income tax return, as both forms declare the same information, but in a different way.

As you may already know, through your income tax return we detail and list all the incomes we have received during the year. Of course, this income has been generated by the assets and rights that we own; including those that we have abroad and that we include in model 720.

Hence, it is very important that the information in both models matches.

That is why we recommend that if you use the services of an accountant for filing your taxes, use the same expert for both models.

At Balcells Group we can provide tax advising help and present both models for you, making sure that you comply with all the deadlines and all the tax obligations according to your particular case, without you having to worry about anything!

Who should file model 720?

As a general rule, both individuals and legal entities that are tax residents in the Spanish territory (i.e. who spend more than 183 days a year in Spain) must submit this form.

This also includes foreigners under the Beckham Law tax regime.

But, in addition, the law establishes that permanent establishments, joint property entities, and civil companies (as well as other institutions detailed in Article 35.4 of the general tax law) must also do so.

However, there is one exception.

As long as the balances or amount of assets/income for any of the 3 blocks we have seen until the 31st of December or the average balance during the last quarter does not exceed € 50,000 euros, you don’t need to present this model.

So, as you can see, this exception works independently within the three mentioned blocks of assets/rights (bank accounts, financial securities, and real estate). If in one of the three you exceed these 50,000 euros, you will have to file this tax declaration. But if you don’t reach that amount in any of them, there is no need.

Submission deadline

The submission deadline for the 720 tax form is from the 1st of January to the 31st of March (always including your asset information on the following year).

This form must be sent to the tax agency, and can be done online with a digital certificate or electronic ID card, through this link.

And should you prepare and submit it every year?

No. Suppose that in the year 2020 you already filed your 720 model. Must you file it again in 2021?

You will only need to do so if the average balance or joint balances on the 31st of December has increased by € 20,000 with respect to the previous declaration.

That that applies to the three blocks seen independently.

In addition, if you experience any asset/right cancellations in any of the 3 blocks, you must also resubmit the model.

What happens if I do not present the form 720 in Spain? Penalties

If you are a tax resident in Spain and have assets or income worth more than € 50,000 abroad, it is absolutely essential that you present this model.

Because the monetary sanctions that the government can impose on you are totally high.

These penalties can be applied whether you do not present the form on time, if you do not present it at all, or if you lack information or have not filled it properly.

If you do not submit the model, the minimum penalty is € 10,000 (€ 5,000 for each piece of information or set of information not declared).

In the case of an untimely declaration without prior requirement, the penalty will be € 100 for each data or set of data not declared or for each erroneous data.

Furthermore, if the tax authorities discover any undeclared assets abroad, there is an additional financial penalty of 150% of the tax liability resulting from the regularisation of the capital gain not included in the form. This is in addition to having to pay unpaid capital gains tax after not declaring it (which ranges from 19 to 23%), plus interest for late payment (3.75% per year).

As you can see, it is essential to present this model on time and to present it properly. That is why we suggest you let our team of accountants and economists take care of everything for you. We will advise you on what to include in the declaration, and prepare all the documents so that you don’t need to worry about anything.

Book a consultation with one of our lawyers and solve all your doubts:

At Balcells Group we have been foreigners effortlessly moving to Spain for over 11 years. We help expats from all around the world with their immigration, business, tax and legal needs; ensuring a legally safe and enjoyable transition to the Spanish territory. Our multilingual team understands the importance of adapting to the cultural and legal specificities of our international clients. We offer a comprehensive service that combines the expertise of several generations of lawyers with the innovation needed to address today’s legal challenges, always striving to simplify processes and ensure reliable, effective results.