Whether you are a self-employed individual (freelance) or a company, sending invoices to your clients will be essential. That’s the way to justify and to get paid based on the products sold or services performed. However, many companies or individual workers are either not very clear on how to do this, or do not include everything they should. But this article will show you exactly how to invoice and what to include in each of your invoices in Spain.

What is an invoice and when should you issue one?

As obvious as it may seem, let’s start from the beginning. An invoice is the document that you must send to your customers in order to get paid for the products sold or services rendered.

Thus, the law requires the creation of this document after any type of transaction with each of your customers.

Through them, you must include not only the amount of the products or services sold, but also the applicable VAT and income tax deductions. In later sections, we will look at each of those elements in detail.

At the end of the quarter, you must collect all the invoices sent to your customers (in addition to those you have paid) and send them to the tax authorities. You can learn more about how tax returns work by being self-employed here.

Also, remember that you must keep your invoices for at least 4 years, because in case of an inspection by the Tax Agency, it will be essential to provide them.

What should you include on your spanish invoices?

Let’s move on to the most important point. Any invoice, in order to be valid, must include the following elements:

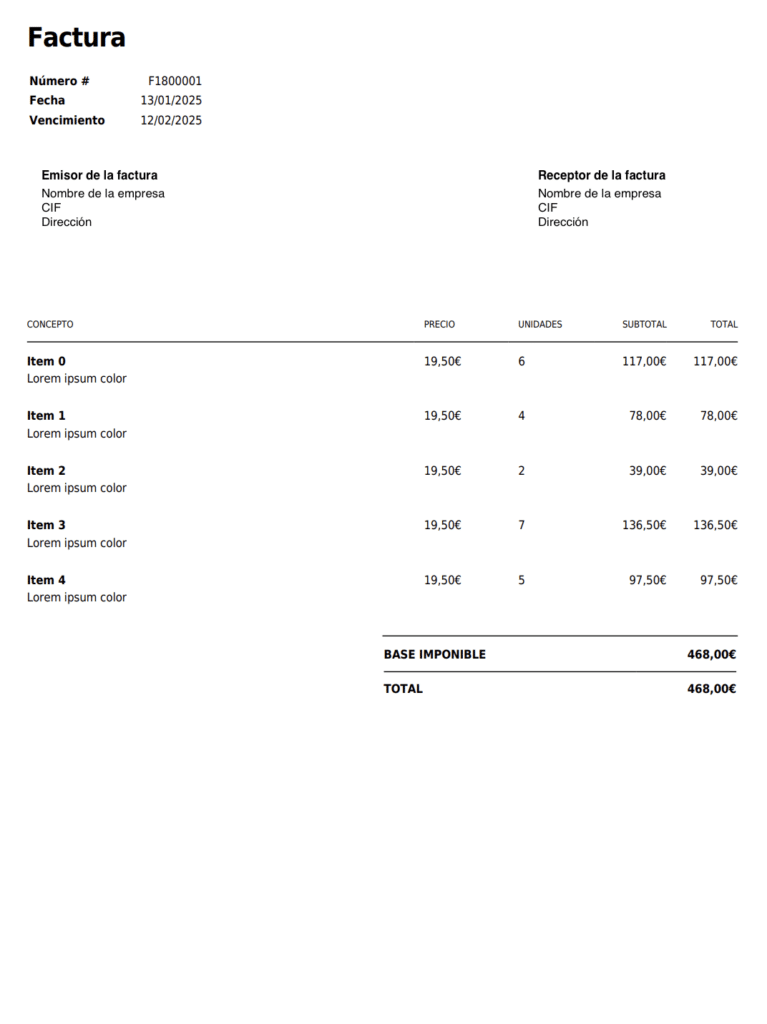

Invoice number

Each invoice must be assigned a unique and independent number that is different from the numbers in any other invoice.

That is, every time you issue a new invoice, you will assign it a number (say 1). The invoice that comes next by date will have the following number (in this case, 2).

Keep in mind that there can be no jumps in the numbers or that an invoice with a later number has an earlier date. This means that an invoice submitted in February 2020 can’t have an invoice number that is lower than an invoice submitted in January of that same year.

As for the format, you can add suffixes to it, such as the current year or fiscal year (2026 + invoice number).

Invoice date

Another important field is the date of the invoice. This must correspond to the issuance date. That is, the day you send the invoice to your customer.

Name of both parties

You will also need to identify both the receiver of the invoice (your client), and the sender (you).

Thus, you must indicate, at the top, the name of the company in the case of a registered business, or name and surname in the case of a self-employed worker.

In the case of a company (either you as the issuer or the client as a recipient), it is important to indicate the acronym corresponding to the type of company (S.L., S.A., etc.).

You must use one column (left) for all the data corresponding to the receiving client; and the one on the right for yours as the sender of the invoice.

Tax identification number

Right after the name of the company or self-employed individual, the tax identification number must be added.

In the case of a company, this will be their CIF, and in the case of a self-employed worker the DNI or NIE number.

Company address of both parties

The third and last line inside the sender and receiver data (in their respective columns) is the company address. That is, the complete address where the activity of both is located (street, number, floor, postal code, city, province, and country).

Description of the operation

In this section you will have to create a table with the following concepts or columns:

- Name of the product sold or service provided

- Unit price

- Final price (without taxes), which is known as the base rate

- VAT is applicable. If there is more than one, you will have to break down the taxable bases according to the VAT rates, as you should bear in mind that some products are taxed at a different rate than the general rate, which may be 0.4 or 10%.

- Personal income tax retentions, which are usually 7% during the first two years of business activity and 15% afterwards. If applicable (which won’t always be the case), you must include it in this table document.

Totalization

Through the table above, you will have added different rows in relation to the different concepts or products invoiced (each one with its corresponding row); adding their price without taxes, corresponding VAT, and retentions.

In this section, located at the bottom of the previous one, you will have to total all these numbers.

That is, add up all the taxable bases, all the VAT, and all the withholdings.

Once the operation is done, you will add it to generate the total of each item of the invoice, and you will make the total calculation to obtain the total amount to be paid by the client to you (which, remember, is obtained by adding the VAT to the taxable base and subtracting the income tax retentions).

Here’s an example so that you can see those different sections on an actual invoice:

Invoice conditions

Finally, in the lowest part of the document, you will include all the conditions corresponding to the invoice.

We are talking about its due date, the payment method (bank details), etc.

Should VAT be applied to all invoices?

No. Whether or not VAT should be applied depends on the client to whom you have provided services or sold products to.

In the case that this client is inside Spain, then you must include the corresponding VAT no matter what (as long as the product or service required to apply one).

However, if the transaction takes place with a customer within the European Union who is VAT registered, then you should not add it.

However, we recommend that you consult one of our tax lawyers to confirm this. Simply send us an email to [email protected] and we will respond within 24 hours.

Here you can also find a complete guide on how to invoice to European Union countries.

What is an amendment invoice?

Suppose you have issued an invoice to your client, but it contains an error or does not comply 100% with the law. For example, there was a mistake in the calculation of the VAT or withholding percentages, or some key element was missing.

In those cases, you must issue a corrective invoice to correct the original.

You must assign a special extra numbering to it (not the same as the original invoice). And you should only carry out this procedure if the invoice is wrongly issued for a quarter prior to the current one, for which you have already declared and paid VAT.

The Spanish Tax Agency will return the corresponding part of the VAT to you.

What should it include? It is very straightforward. It must be the same as the original invoice already issued with an error, but corrected.

Can you send invoices by mail? Electronic invoice

This is certainly a very controversial issue.

Is it possible to send invoices by email in Spain? Do they have the same legal validity?

After the approval of the new Invoicing Regulation in 2012, it is entirely possible to do so, under what is known as electronic invoicing.

The only thing you have to take into account is that the recipient must have given his consent to receive the invoice by telematic means. Apart from that, and as long as the content is original, authentic, and contains all the elements that we have mentioned, there will be no problem.

However remember, you can also send it in physical paper format.

Do you still have questions? Our team of tax experts is waiting to help you as soon as possible.

Book a consultation with one of our lawyers and solve all your doubts:

At Balcells Group we have been foreigners effortlessly moving to Spain for over 11 years. We help expats from all around the world with their immigration, business, tax and legal needs; ensuring a legally safe and enjoyable transition to the Spanish territory. Our multilingual team understands the importance of adapting to the cultural and legal specificities of our international clients. We offer a comprehensive service that combines the expertise of several generations of lawyers with the innovation needed to address today’s legal challenges, always striving to simplify processes and ensure reliable, effective results.